Grandparenting and Financial Assistance to Grandchildren

(FS1983, Review October 2025)Contact your county NDSU Extension office to request a printed copy.

NDSU staff can order copies online (login required).

Grandparents are known for their generosity during holidays, birthdays, vacations or times of need. Many grandparents today are helping financially more than in the past.

Not only has the assistance from grandparents increased, the average age of grandparents today is significantly lower than in the past. This publication explores issues related to grandparents providing financial assistance to grandchildren, financial decisions and some helpful resources in this process.

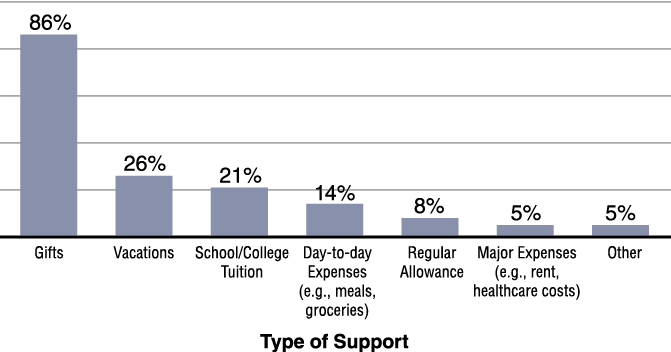

What are Grandparents Paying For?

What Are Grandparents Often Paying For?

- Birthday or holiday gifts

- Day-to-day expenses

- Vacation costs

- Life events (wedding, etc.)

- Mortgage or rent

- Health care

- Child care

- Education costs

- Other needs

Learning Financial Literacy Together – A Goal Setting Exercise

Giving money to your grandchildren can be a fun and interactive learning experience. Instead of just passing on money, setting a good financial example and teaching healthy financial practices are important elements of extending financial help to grandchildren. You can teach financial lessons to a grandchild whether you have a limited, moderate or high income.

To get started, set some financial goals for yourself and your grandchildren. As an example, for some families who like to take family trips, this could be a great time to involve the grandchildren in all the costs and planning. Another way you might involve your grandchildren could be through helping them plan for and assisting with a bigger purchase, such as a bike or even a car.

Working together with your grandchildren provides an opportunity to teach them the process of setting and reaching for financial goals. In turn, this can set them up for a better understanding of their own finances.

Getting the Grandkids Involved with Finances

- Matching funds to purchase an item or save for a purchase can get them motivated and excited! Put up $5, $10, $50 or $100 to match that amount when they are ready.

- Give to a charity the family supports or a grandchild wants to support. Study it together.

- Establish a savings account at a local financial institution with a grandchild and make a contribution to it.

- Turn a financial gift into a lesson by going to the store with them to purchase what they want. Talk about the costs and give them opportunities to put some of the gift into their savings.

- Teach your grandkids to use the “three envelopes rule” for cash gifts: one for saving, one for sharing with others and one for spending. Also, teach them to figure out if a future purchase is a want or a need.

- Use the time spent together to assess financial goals and make some plans to pursue financial well-being.

Brainstorm some finance experiences where you could involve your grandchild(ren). Be creative! Write down two or three.

- __________________________________________________________

- __________________________________________________________

- __________________________________________________________

Your Money, Your Grandchildren

Being a grandparent gives you many opportunities to be generous in your gift giving. It also gives you the ability to teach your grandchildren financial skills, which will prepare them for the future. Grandparents want a positive future for their grandchildren and assisting with finances can be one pathway to brighten that future.

Being aware of your own financial situation in regard to retirement, savings and investments will allow you to be smart about the money you are passing on to others. Set goals that fit with your specific needs, interests and circumstances. Take your finances seriously and help your grandchildren learn how to value money and learn skills to manage it well for a better future.

References

AARP Research. (2019). Money and the modern grandparent. Washington, D.C.: AARP Research. Online at: www.aarp.org/content/dam/aarp/research/surveys_statistics/life-leisure/2019/aarp-grandparenting-study-money-fact-sheet.doi.10.26419-2Fres.00289.017.pdf

Beach, B. (2013). Grandparental generosity: Financial transfers from grandparents to grandchildren. London: ILC-UK. Online at: https://ilcuk.org.uk/wp-content/uploads/2018/11/Grandparental-Generosity.pdf

Harrington Meyer, M., and Abdul-Malak, Y. (Eds.). (2016). Grandparenting in the United States. New York: Baywood Publishing Co.

Heath, S., and Calvert, E. (2013). Gifts, loans and intergenerational support to young adults. Sociology, 47(6), 1120-1135.

Metlife Mature Market Institute. (2012). Grandparents Investing in Grandchildren: The MetLife Study on How Grandparents Share Their Time, Values, and Money. New York: MetLife Mature Market Institute and Generations United. Online at: www.gu.org/app/uploads/2018/05/Intergenerational-Report-MMMI-Grandparents-Investing-In-Grandchildren-Study.pdf

Palisades Hudson Financial Group. (2019). Looking ahead: Life, family, wealth and business after 55. Kindle Direct Publishing.

Scharmer, L. (May 2013). Taking charge of family finances. Extension publication FE222. Fargo, N.D.: NDSU Extension.

TIAA Individual Advisory Services. (2019). Saving for college and financial aid options. New York: Teachers Insurance and Annuity Association of America-College Retirement Equities Fund. Online at: www.tiaa.org/public/pdf/college_savings_and_finanical_aid_options.pdf

U.S. Securities and Exchange Commission. (2018). Investor Bulletin: 10 Questions to Consider Before Opening a 529 Account. Online at: www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins-10

This publication was authored by Carrie Johnson, Ph.D., Personal and Family Finance Specialist, NDSU Extension; Sean Brotherson, Ph.D., Family Science Specialist, NDSU Extension; Meghan Yerhot, M.S., Extension Associate, NDSU Extension; and Franchesca Cortez, M.S., 2020.

For more in The Art of Grandparenting series, please visit www.ndsu.edu/agriculture/extension/extension-topics/family

North Dakota State University, Fargo, North Dakota

The NDSU Extension Service does not endorse commercial products or companies even though reference may be made to tradenames, trademarks or service names.

For more information on this and other topics, see www.ndsu.edu/extension

County commissions, North Dakota State University and U.S. Department of Agriculture cooperating. NDSU does not discriminate in its programs and activities on the basis of age, color, gender expression/identity, genetic information, marital status, national origin, participation in lawful off-campus activity, physical or mental disability, pregnancy, public assistance status, race, religion, sex, sexual orientation, spousal relationship to current employee, or veteran status, as applicable. Direct inquiries to Vice Provost for Title IX/ADA Coordinator, Old Main 100, 701-231-7708, ndsu.eoaa@ndsu.edu. This publication will be made available in alternative formats for people with disabilities upon request, 701-231-7881. 600-9-20; w-10-25