Potential for Drought Can Impact Prices and Marketing Plans

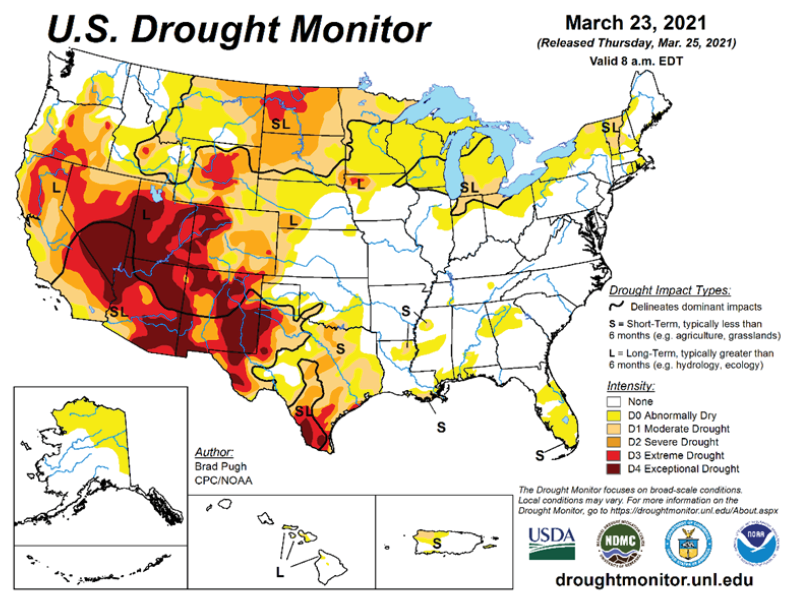

The most recent U.S. Drought Monitor, prepared by the National Drought Mitigation Center at the University of Nebraska, shows that North Dakota, most of South Dakota and northwestern Minnesota are experiencing some level of drought conditions. Given tight 2020-21 ending stocks, the grain markets will be watching drought conditions and weather forecasts more closely than normal this year.

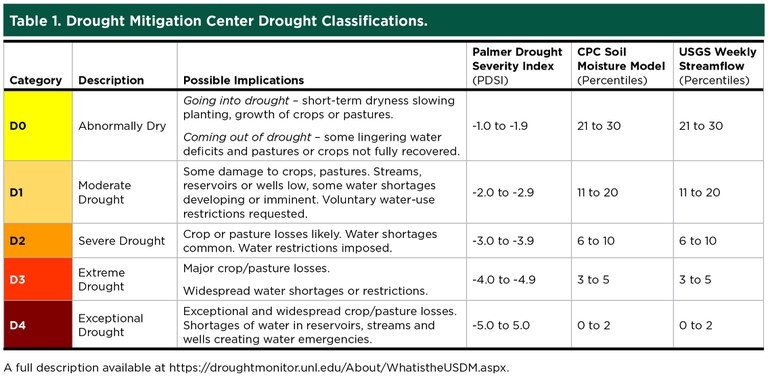

However, I am concerned that the information provided by the Drought Monitor maps is being misinterpreted. The Drought Mitigation Center uses a color-coded drought category rating ranging from D0 to D4. Table 1 summarizes some of the key measurement criteria used to define each category.

A rather simplistic way to view the drought categories is to consider how deep the drought has reached within the soil profile. As the drought moves from category D1 to D2 or D3, the drought conditions move from the surface into the deeper soil layers.

The critical questions for crop yields are how much moisture is available within the root zone, temperatures, the timing of rainfall and crop water needs. Drought conditions do not always result in dramatically lower yields, but well-timed rains and favorable temperatures are needed to maintain yield potential. This is especially true during plant flowering and seed development, when plant water use is high.

Localized drought conditions also can create problems for developing or adjusting farm-level marketing plans. The worst situation for net farm income is to have farm-level yields that are just above crop insurance guarantees, combined with above-average production at the national level, that result in lower overall market prices.

The temptation is to think that because you have drought conditions on your farm, national prices should respond and move higher. In reality, significant drought conditions must impact a large enough area

to raise concerns about total supplies.

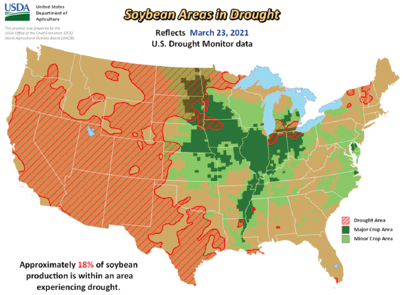

For example, based upon the March 23, 2021, U.S. Department of Agriculture – U.S. Agriculture Drought Monitor, approximately 20% of corn production, 18% of soybean production, 24% of winter wheat production and 78% of spring wheat production are experiencing drought conditions.

Let’s look at the potential prices response to drought conditions by comparing soybeans and spring wheat. Approximately 18% of potential soybean production is experiencing drought conditions. However, the projected soybean stocks-to-use ratio, ending stocks divided by total use, for the 2020-21 marketing year is 2.6%, which is equal to the record low set in 2008-09.

Soybean prices likely will be very sensitive to spring and summer weather forecasts. If drought conditions spread and more key productions regions are impacted, very few bushels are available in storage to offset lower yields.

In contrast, the spring wheat market is evaluating the opposite situation. The 2020-21 marketing year stocks-to-use ratio is 42%, which is above average. But approximately 78% of the potential production is experiencing drought conditions.

The odds of below-average yields are strong because of the dry soil conditions, but last year’s large inventories can help compensate for lower production this year. The spring wheat markets will be watching weather conditions very closely, but extended dry conditions may need to occur before prices will respond to production concerns.

Local drought conditions can make developing a marketing plan very difficult. New crop market prices are often strong in early spring, trying to influence farmers’ planting decisions. However, farm managers are reluctant to forward contract for harvest delivery because they don’t know how many bushels can be produced. Farm managers struggle to balance production risk, or lower yields, against price risk, or lower prices.

One approach used to balance these risks is to divide your marketing plan into three time periods: preplant, midsummer and postharvest. The amount of grain priced during each of these periods can change from year to year.

For example, given today’s drought conditions in North Dakota, the amount of grain priced during the preplant window may be lower than normal (for example, 15% to 25% of expected production). Additional sales can be made in midsummer, when you can more accurately estimate yield potential and have more information about national production estimates (for example, price an additional 20% to 30% in June or July). The remaining production can be priced after harvest, when final yields and quality are known.

Once again, the amount of grain priced and price targets for each of these three periods can be adjusted from year to year, depending upon weather and market conditions, and may change by crop.

-Frayne Olson, NDSU Extension Crop Economist/Marketing Specialist